Representative image of patrons at a natural history museum. Photo: Allison Meier/Flickr (CC BY-SA 2.0)

The year 2020 was supposed to be the year that governments, business leaders and civil society came together to report back on the past decade’s worth of progress on addressing the biodiversity crisis. But the COVID-19 pandemic intervened and most of the big meetings scheduled for 2020 were scaled down or postponed until 2021. But that doesn’t mean 2020 hasn’t been an eventful year for biodiversity conservation efforts. Perhaps most significantly, COVID-19 has prompted a reevaluation of our relationship with the world around us, including how we interact with other species and their habitats.

According to Simon Zadek, chair of the Finance for Biodiversity Initiative, the pandemic may ultimately come to be seen as a tipping point in long-running efforts to persuade the financial sector to factor nature and biodiversity into decision-making. In recent years, incorporating carbon emissions into financial decisions had become mainstream among corporations, governments and development finance institutions (DFIs), but biodiversity remained a remote, esoteric consideration. But COVID-19 changed that.

Zadek recalls a meeting he had in January 2020 with a group of financial institutions to discuss integrating nature-based metrics and data into frameworks and standards. Their response, according to Zadek, was they had already expended all their political capital persuading decision-makers on the need to account for carbon. They could not “now tell them that they need to look at nature too.”

Ten months later that same group was “about to produce a major piece of work on how to advance the data and metrics in measuring nature-related risk dependencies and impacts of financial institutions,” Zadek said. “We’re seeing a rapid pathway arc of acceptance that nature is the next in the tube … so that financial institutions can get really an understanding what those risks, dependencies and impacts are.”

With natural ecosystems being rapidly degraded and destroyed, as evidenced by the catastrophic fires around the globe this year, this shift was welcome news for Zadek, who’s been working to drive systemic change among financial institutions, governments and corporations for the better part of three decades. These efforts began with governance, labour and human rights, but have lately come to focus on getting public finance aligned with climate goals and nature stewardship.

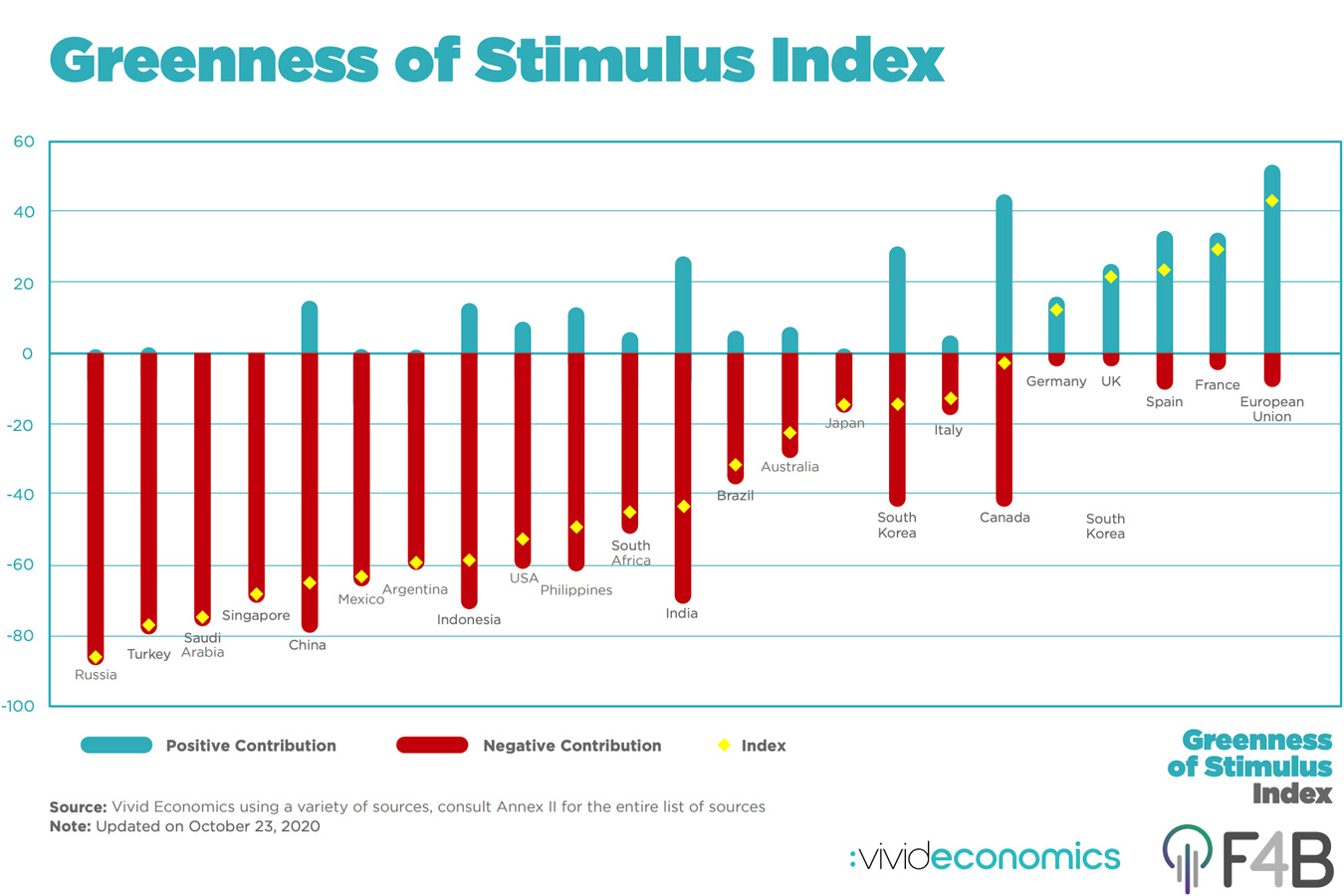

In his current role as chair of the Finance for Biodiversity Initiative, Zadek has led a campaign to get biodiversity impacts incorporated into public and private sector financial decision-making. This effort takes a multi-pronged approach, including market innovation, accounting for biodiversity-related liability, integrating biodiversity policy into financial frameworks, public-facing campaigns, and analysing how governments are responding to the COVID crisis. On that last point, the Finance for Biodiversity Initiative publishes a “Greenness of Stimulus Index” that evaluates the ecological sustainability of COVID stimulus programs.

“Finance for Biodiversity has done a rating, turning stimulus commitments into an index of the nature friendliness,” he said. “The results are not very positive.

“We’ve covered all of the G-20 countries and all of the European countries plus a few more and the bottom line is that only three or four countries have stimulus programs strongly linked to nature and climate. The vast array of those stimulus programs are either neutral or negative.”

Zadek says aligning global finance with nature conservation and restoration would bring transformative change that goes far beyond what conservation groups themselves can do alone.

“The conservation community tends to think about finance in terms of finance for conservation. That is, ‘How can we raise money to spend on conservation.’ That is a completely legitimate activity but it is ‘small beer,’” he said, noting that there are $350 trillion worth of financial assets in private capital and financial markets as well as $25 trillion to $30 trillion worth of annual public finance spending. “We need to move away from this rather narrow focus on raising money to spend on conservation and realize that it’s these far larger numbers that are really shaping nature outcomes.”

Zadek discussed these issues and more during a November 2020 conversation with Mongabay founder and CEO Rhett A. Butler. The interview below has been lightly edited for clarity.

An interview with Simon Zadek

Rhett Butler: I’d love to hear a little about your background in terms of what motivated you to get involved with sustainability?

Simon Zadek: Sure. Very pleased to be with you here today. Right now, I’m the chair of an initiative called Finance for Biodiversity (f4b-initiative.net) and we’ll come back to that in a few minutes. In our earlier conversation, we chatted about how I got into this. Of course, it depends how far back you go since I’m many decades into my life but I would say, what kicked me off is a book. It was a book written by a guy called Anthony Samsung, back in the ’60s called The Sovereign State of ITT. ITT, as you’ll probably know, was a very important U.S. telecommunications company and The Sovereign State of ITT was effectively a journalist’s book on the lack of accountability of large corporations. I got into the sustainability space through an accountability lens, ethics and justice rather than, for example, environment and climate, and it’s only really in the last eight, nine years that I’ve significantly swung from a focus on social and economic aspects of human justice issues and labor standards issues into environmental climate and now, nature. I’ve come to that somewhat late in my work, having come from that corporate accountability background originally.

You just came out with a report that spoke to development finance institutions. What were your top takeaways from that report? And what actions would you hope development finance institutions take after seeing that report?

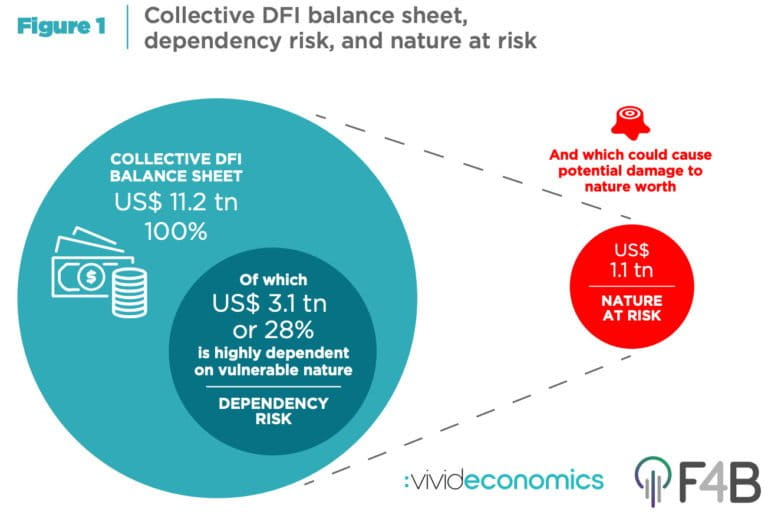

President [Emmanuel] Macron [of France] and [U.N.] Secretary-General [António] Guterres co-hosted a meeting [earlier in November] called Financing in Common which brought together for the first time the world’s development finance institutions. By their measure, there are 452 such institutions, obviously many different sizes and approaches with a combined balance sheet of $11.2 trillion. Just to put that in perspective, total global capital markets, financial capital markets amount to about $350 trillion. So, it is not an insignificant amount.

It’s a lot of cash, in fact. We did a piece of work that asked the question quantitatively for the aggregate balance sheet of all of these DFIs. (“Aligning Development Finance with Nature’s Needs”) To what extent is their lending dependent on vulnerable nature and can we quantify financially the nature at risk as a result of their lending practices? And of course, all of these numbers are fairly high level and are subject to margins of error, but the answer to both questions was yes, and we found that for over a third to a half of the group, the overall balance sheet was highly dependent on vulnerable nature. Ecosystem services were being drawn on and often not paid for in order to make those loans profitable or useful for those who had borrowed the money, and we found that nature at risk of that $11.2 trillion amounted in our estimate to about $1.1 trillion worth each year, out of a total of about two and a quarter trillion dollars lending each year.

Whether the number is 100 million that way or 100 million the other way, it doesn’t really matter. The core of the story is the world’s most progressive development finance institutions are highly dependent on vulnerable nature and play significant nature at risk through their lending practices. So, then you come on to, what on earth is going on, and the answer is even many of those DFIs have embraced at least the mitigation side of climate change and do climate stress tests of their balance sheets. There are few that go beyond individual project analysis and doing a balance sheet-wide analysis of where nature fits into what they do.

Our first and foremost recommendation, perhaps a little geeky, is that every DFI in the world needs to stress test their balance sheet for how dependent they are on vulnerable nature and what nature they put at risk. So, analysis of really where nature fits into their lending portfolio, and they need to report on that publicly and we think, since almost all of these DFIs are in various ways owned by governments, it should be government policy that needs to be increasingly progressive in terms of zero net loss or positive that drives these DFIs to really align those policy frameworks with how they’re approaching the nexus between nature and lending.

You mentioned an important qualifier which was “progressive” DFIs. Do you see opportunities with DFIs in places like China which obviously is making big investments in the Belt and Road Initiative?

Progressive can mean many different things, obviously, but you’re right to question the range across different jurisdictions and types of public development banks, if you like, or DFIs. The Chinese development bank at this point, I’m right in saying, has the largest balance sheet of any DFI on the planet and clearly that is only one of a number of Chinese financial institutions that are linked to strong policy mandates including, obviously, the AIB, but also some of the state-owned banks and state-connected asset management companies.

Clearly, they represent a significant source of financing across the Belt and Road and that has huge implications for what development will happen down that massive swath of countries that in 20 years’ time, if left unchecked, we’ll have the highest level of carbon emissions of any other part of the world, that group of countries in aggregate. And so, clearly, pushing Chinese financial institutions — who, remember, are often collaborating with many other financial institutions from the West and elsewhere — pushing them to take nature and broadly climate into account is really critical.

The opportunity is there because the Chinese government clearly has an interest not only in contributing to the public good but also ensuring that their lending does not lead to either poor political or reputational outcomes or indeed delinquent investments that fail because of their co-dependency on vulnerable nature, that doesn’t stand up to the stress. Progress is absolutely possible but very challenging, if one is trying to build international cooperation at a time where the conflict between China and other parts of the world is clearly on the rise.

On the conflict issue, living here in the U.S. for the past four years has felt like a lost period for progress on climate and biodiversity conservation and I’m curious as to where you see the most action occurring right now in terms of advancing these ideas?

It depends what your metrics are, inevitably but let’s look at the largest flow of public finance, just for a second. In a short period of time, in the history of civilisation, that is clearly the stimulus programs that have been announced in the context of COVID and that have flowed to the tune of, or commitments to, about $12 trillion moving rapidly across the global economy particularly, obviously, in larger economies, both so-called developed and larger emerging economies like, Brazil, South Africa, China, India, Malaysia and so on.

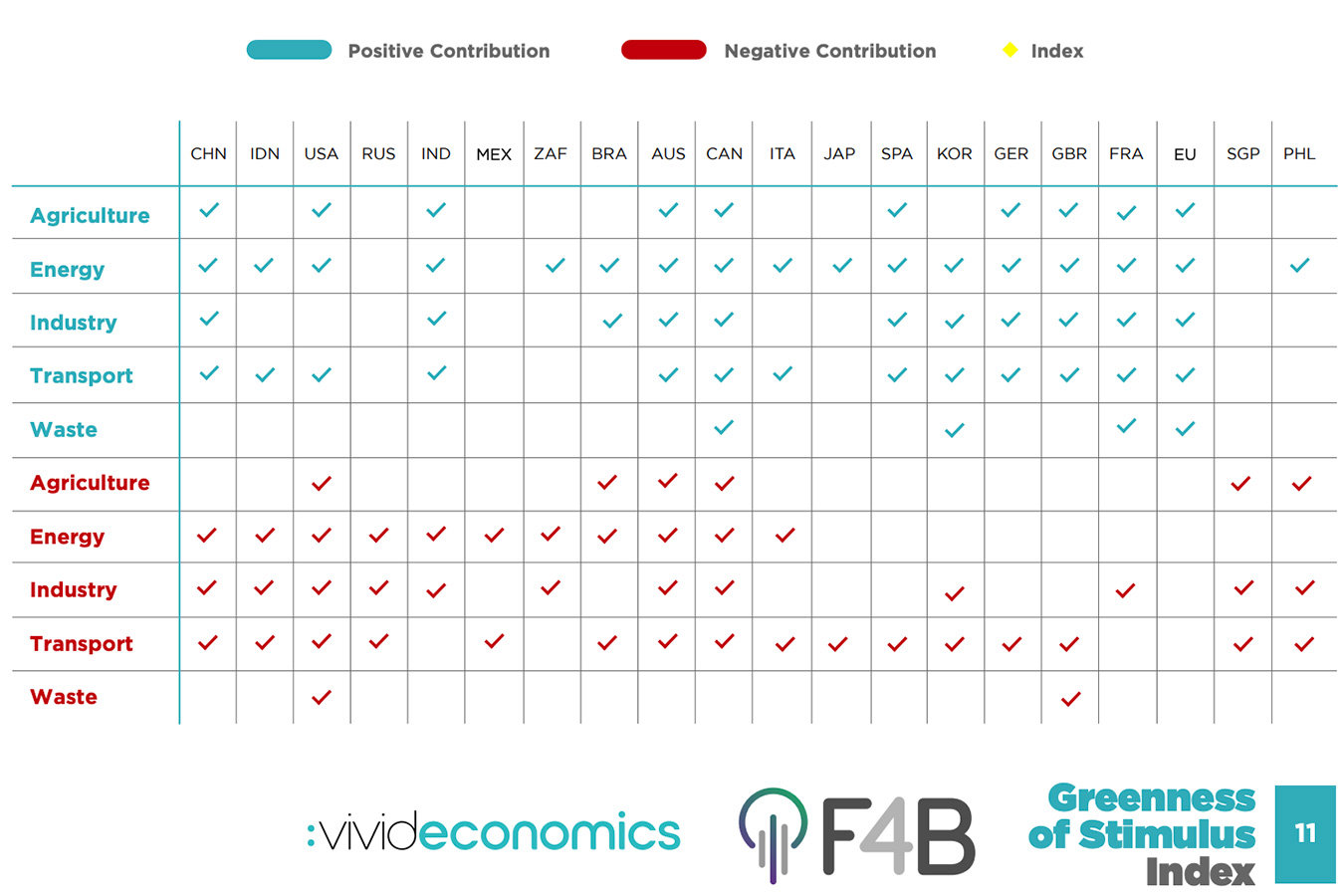

Finance for Biodiversity has done a rating, turning stimulus commitments into an index of the nature friendliness, if you like. (“Greenness of the Stimulus Index”) Not so much of the flows themselves, which are harder to track, but of the commitments that have been made. In other words, how much money and what the plan is as to how to spend that money. The results are not very positive. We’ve covered now about $4 trillion or $5 trillion of stimulus. We’ve covered all of the G-20 countries and all of the European countries plus a few more and the bottom line is that only three or four countries have stimulus programs strongly linked to nature and climate. The vast array of those stimulus programs are either neutral or negative, not necessarily deliberately negative but because of bailouts of, for example, fossil fuel or transport-intensive industries.

We see perhaps the usual suspects, so the likes of the U.K., other parts of the EU that have tended to have a stronger green in their policy commitment associated with their stimulus programs. But really, across the board, it is a very poor showing. So, one doesn’t have to look at some grand theory of finance or every corner of the global financial system, we can look at this tsunami of money that is moving at the moment and already see policy-driven finance where really not enough is being done to ensure green outcomes.

I noticed the two countries that Mongabay covers a lot, Indonesia and Brazil. Both scored fairly poorly on the index in terms of the stimulus.

I could just go yes, you’re right and leave it at that. Obviously, it is very difficult to compare. I don’t know, Belgium with Indonesia, these are almost on different planets in terms of the economies they have, the level of wealth they have, the extent to which they can actively intervene in carbon emission-related industries or indeed, actively intervene in the way in which nature is being impacted. Frankly, Belgium doesn’t have a lot of nature left and is largely a service-driven country, and Indonesia has huge swaths of nature which are complex at multiple levels both biologically or scientifically and also in terms of how they’re being used across the board.

It’s fine doing an index. It demonstrates a piece of the story but one shouldn’t get too refined. It shouldn’t come as a surprise to us that Indonesia and Brazil perhaps struggle most or more than others to really figure out how stimulus programs that really need to be focused on bringing out people out of poverty very quickly, may not pay sufficient attention to the green side of the story. But perhaps that changes as we move from stimulus to recovery. When we start thinking about recovery — once talking about somewhat longer-term financing, not emergency money out of the door to enable people to buy food — there one would expect the likes of Brazil and Indonesia to step up to the plate and really show that there are structural transformation drivers built into the way in which they’re financing the recovery.

How do you drive that change toward a greener finance?

Multiple routes. Obviously, it is a set of policy drivers that determine largely where public financing goes. Let me perhaps turn to a different part of global finance, which is debt and, specifically, sovereign debt. As those who follow the news at least in the financial press will be aware. The pandemic has brought with it not only economic chaos and downturn but also a growing crisis in the sovereign debt market and in particular in sovereign debt that has effectively developing countries as debtors. Their exports have collapsed. They are struggling to move their economies forward and yet they have debt repayment schedules that lead to the potential of debt failure.

So, just being unable to pay their debts with all longer-term implications for those countries being able to access international capital markets in the future. What’s interesting is that over the last three months, we have seen a number of initiatives emerging that are trying to connect the dots between debt relief and debt restructuring on the one hand, sovereign debt and what it takes to use some of those funds unlocked to enhance climate and nature outcomes. Now, on the negative side that can be framed and seen as just a new form of conditionality. We’re open to providing debt relief, if you do X, Y, Z on the green and biodiversity side.

Clearly, there will be pushback. and sometimes rightly [so], if funds unlocked through debt relief are being forced into nature investment rather than, for example, helping people who are on the brink of starvation. That would clearly be a catastrophic approach. At the same time, it does seem possible that in the context of what may be significant debt relief that is provided to a growing number of developing countries, deals can be made, where financing can be linked not only to the immediate need to help people but also that longer-term transition that will boost economic productivity because it reduces carbon emissions and supports the role of natural capital in driving prosperity. And we’ve never really seen that play out in so-called Paris Club of Sovereign Creditors or discussions happening at the IMF and elsewhere.

So, this is really the first time deals like this is seriously being discussed. The forthcoming presidency of the G-20 will be held by Italy, starting from the first of December. So, in a few days it will be an important venue where this discussion happens and if it moves constructively then we could have a situation where we can find that sweet spot between making significant debt relief and moving forward. So, alleviating short-term pain and, at the same time, unlocking finance that can support that green transition that we’re all understanding that needs to be paid for and needs to happen at scale.

In the reports you’ve been associated with, you’ve mentioned the idea of an instrument called the Nature Performance Bond. Could you elaborate a little on that?

Those working in the nature finance nexus, we’ll almost certainly know a lot about nature debt swaps and there’s a fairly long history of nature debt swaps, which is when somebody holding a bit of debt of say Gabon, Suriname, the Seychelles, or somewhere else says, “We’re willing to forgive X million pounds’ or dollars’ worth of debt if you agree to spend that money on saving the rhino or increasing tree coverage or something of that kind.” That’s a debt nature swap. And while these need to be celebrated for unlocking money for nature, they have remained rather ad hoc, rather small scale, and have not always proved very satisfactory in terms of the data or how the money has to be spent. Also, the creditor that they’ve given debt relief to and perhaps the performance outcomes that were agreed for the future don’t always come true. (“Recapitalising Sovreign Debt – why nature performance bonds are needed now – policy paper”)

Interesting experience but not terribly satisfactory. So really, the question is, where do we go from here, and we’ve learned since 2011 which is when the green bond market started. That standardisation is really important, that one needs to develop taxonomies and guidelines and standards and certification models that allow one to move from an ad hoc place — a little bit here and a little bit there, where everything is always negotiated uniquely — to a more scaled approach. And ultimately, the world’s capital markets operate through standardisation, where credit risk can be more precisely analysed, where different types of levels of risk of assets can be bundled effectively and so on. We can move away from debt nature swaps and move into what we’re talking about, which is nature performance bonds, which combines two different possible characteristics.

One is a use of proceeds bond, so that’s like a green bond. I promise to use the money on X, to what in the jargon is called a State Contingent Debt Instrument, which isn’t a state in terms of a country but is the state of something in terms of the condition. In other words, you have to pay X interest rate, unless you achieve this performance outcome, in which case you pay less interest rate. And we began to see so-called SDG-aligned bonds emerging that are not just use of proceeds bonds but state contingent debt instruments. We will deliver that outcome, but in return for that, we will pay a lower coupon on the debt that we raise from you. The nature performance bond is a combination of these two pieces and we feel can play a really powerful role in the context of the debt relief and debt restructuring that we hope will play out over the next year or two.

Looking at the longer term, what would success look like to you, say, 10 years from now in this space?

I hope I will be putting my feet up and not having to do anything at all and I won’t have to have a mask on every time I walk out of the house. I can think of all measures of success, but probably not the ones that you were thinking of. Let’s pick out a couple of pieces, if the umbrella objective is that one syncing to align global finance with nature and climate outcomes. Let’s take that as the North Star or the Southern Cross, if you happen to be elsewhere on the planet. Then what does that look like in a couple of instances? Let’s say, sovereign debt. If you’re running a company and you’re trying to borrow money off me, I’m going to ask to see your balance sheet.

If you haven’t got a balance sheet as visible, I’m certainly not going to lend you any money. But in sovereign debt markets, there are no balance sheets. There are lots of credit rating agencies, but countries don’t have balance sheets, according to the world of finance, and that’s wrong. There are a number of pieces to that balance sheet and natural capital is a critical part of it. In 10 years’ time, sovereign debt markets should always have balance sheets. Natural capital needs to be an embedded part, not just have one instrument called Nature Performance Bonds, but of the entirety of sovereign debt markets that countries should be able to demonstrate social and natural capital balance sheets as well as demonstrate economic and financial solvency.

That’s achievable and we have an opportunity to advance that agenda now, building on some of the work that’s happened over recent years. Secondly, we have the Lords of Finance, if I can call them that, who are not folks running financial institutions but the folks running central banks. It’s the folks who govern the financial system, and today, it’s perfectly possible to have a government that passes a law that says, “We’re going to do this about climate and this about nature.” And for financial institutions not to have to respond because the central bank doesn’t have to follow that policy guidance. The so-called independence of central banks means that they are not obliged to be in lockstep with policy.

Now that has some upsides, independence clearly, but it has some downsides in the context of the green crisis that we’re facing today. We need, not in 10 years but in a far shorter period of time, the world’s institutions that govern finance to be aligned to the policy architecture of the countries in which they are hosted, whether it be the U.K.’s Westminster or Congress or elsewhere. Otherwise, we will have a financial community that has a license to operate, even though it is dramatically at odds with the policies of the countries that are hosting them in practice.

We need to reconnect the dots there, and then I would add, maybe just as a third example, on the public side, the public finance. We live in a digital world now and it is perfectly possible, and we see this in some countries, that if a minister drinks a cup of coffee in a cafe and decides to charge it to the public purse, two days later that is on a website showing what that minister bought, how much it costs and where they were and why on earth it was charged to the taxpayer. Digitalization now allows that really with ease along with all sortable and analyzable tools.

We need public finance to move in that direction. We need to move toward a far more radical transparency and we need to see how green in its various shapes and forms becomes a much more integrated aspect of the way in which public finance works. And again, this is not a weird dream or fantasy that I had in the middle of the night. There are many examples of where this is happening in practice. And yet, when you look at the $25 trillion to $30 trillion a year that constitutes the public finance of the world each year, it’s a tiny portion that is sensitized, let alone transparent, around its alignment to green objectives.

You’re talking about nature which is all encompassing. From my viewpoint, it seems like the finance sector has a decent understanding of climate change now and the externalities associated with it and the fact that we need to cut carbon emissions. But biodiversity always felt like something which is still not totally understood or the valuation models are still lacking. I’m curious to hear your take on that issue and how biodiversity is actually getting attention and receiving financing being valued these days?

Sure. I remember a meeting, I attended in January this year, a different world before COVID broke out. I sat with a group of financial institutions and associations that represent many other financial institutions and I argued the toss with them that they should be leading and looking at metrics and data and frameworks and standards and tools linked to nature, and the response was — this is January — the response was across the board: “Simon, you’re absolutely right, but we are so bound down by the challenges of trying to figure out the climate piece of this and we’ve spent our political capital, persuading our CEO and shareholders that it is reasonable that we are looking at this stuff more carefully, that we cannot roll another ball down the alley right now and tell them that they need to look at nature too.” This was back in January.

That same group of actors 10 months later are about to produce a major piece of work on how to advance the data and metrics in measuring nature-related risk dependencies and impacts of financial institutions. The last 10 months has been, in many way, a surprising uplift journey as the financial community, at least parts of it, have really begun to respond to what many activists such as yourselves have been arguing for decades but largely with little effect. So, we’re seeing a rapid pathway arc of acceptance that nature is the next in the tube, if you like, where the metrics and data and so on need to be figured out, so that financial institutions can get really an understanding what those risks, dependencies and impacts are, and one illustration of that is the recently launched task force on nature-related financial risks.

That spills off the tongue very cute, which is essentially how should financial institutions — what data should financial institutions demand from corporates that are, for example, reporting on stock exchanges, so that they can understand nature-related risks? And some of you will know there’s been an equivalent process called the task force on climate-related financial risks that has been running now for three years, to some considerable success, and I am the co-chair of the technical expert group of this new initiative, called the Task Force on Nature-Related Financial Disclosure. (“The Case for a Nature Related Financial Disclosures”)

There are 70 different financial institutions involved, many governments engaging. It will probably be part of the conversations in the G-7 and the G-20 next year. That doesn’t mean now that this deal is done and that we reached a successful conclusion, but it does mean that we’re breaking through decades of unwillingness to listen and respond, and are beginning to move into how practically these organisations will take nature into account.

The conservation community tends to think about finance in terms of finance for conservation. That is, “How can we raise money to spend on conservation.” That is a completely legitimate activity but it is “small beer,” one would say in England, or “small change” in North America. The real game in play is, how to align global finance? $350 trillion worth of financial assets in private capital and financial markets. $25 trillion to $30 trillion worth of public finance spending every year. The real challenge is not finance for conservation, but aligning global finance with conservation objectives. We need to move away from this rather narrow focus on raising money to spend on conservation and realize that it’s these far larger numbers that are really shaping nature outcomes and the laws that we need to change going forward.

That’s perhaps obvious in what I’ve been saying for the past 20 minutes but it’s a critical message for the conservation community to make that jump into a more systemic view of how we need to approach finance.

Thank you again so much for taking the time. I really appreciate it.

Absolutely, my pleasure. Thank you very much.

This interview first appeared on Mongabay. Read the original here.